Published

Why It’s Time to Mind Europe’s Services Gap

By: Andrea Dugo Erik van der Marel

Research Areas: EU Single Market, Institutions, and Governance Industrial and Competitiveness Policy Innovation, IP, and Human Capital

Speaking at the World Economic Forum in Davos last week, President Trump told Europe it was “not heading in the right direction”. The line was classic Trump: light on evidence, heavy on provocation.

Yet the real story isn’t geopolitical bravado but a widening structural divide between the U.S. and Europe economies. Since 1990, Europe’s share of global GDP has slid from roughly a quarter to just 14 per cent – a long decline that rhetoric alone cannot explain away.

Central to Europe’s loss of global economic heft is not its manufacturing decline, as often claimed, but the part of the economy that rarely draws attention yet will determine its success in the 21st century: services.

From AI architects to bioinformatics and engineers, services employ just as many workers in Europe as in the US. But Europe generates far less output and has struggled to turn services into a true engine of growth.

The EU produces roughly $13 trillion in value-added from services – barely half the US figure. More worryingly, the gap is widening rapidly. Since 2000, US services productivity has soared by 60 per cent. In Europe? Just 10.

A European cloud provider employing thousands of engineers may still generate a fraction of the revenue per worker of a US rival, not because of inferior talent but because underinvestment prevents it from scaling services the same way.

In the US, services now outstrip manufacturing in productivity, generating more high-growth firms and paying higher wages. Put simply, services now deliver broader gains for society.

As Paul Krugman once quipped, productivity isn’t everything, but in the long run it’s almost everything. If this pattern persists, the prosperity gap between Americans and Europeans by 2035 could resemble today’s gap between Europeans and Indians.

What most distinguishes the US – and increasingly separates it from Europe – is its dominance in services innovation.

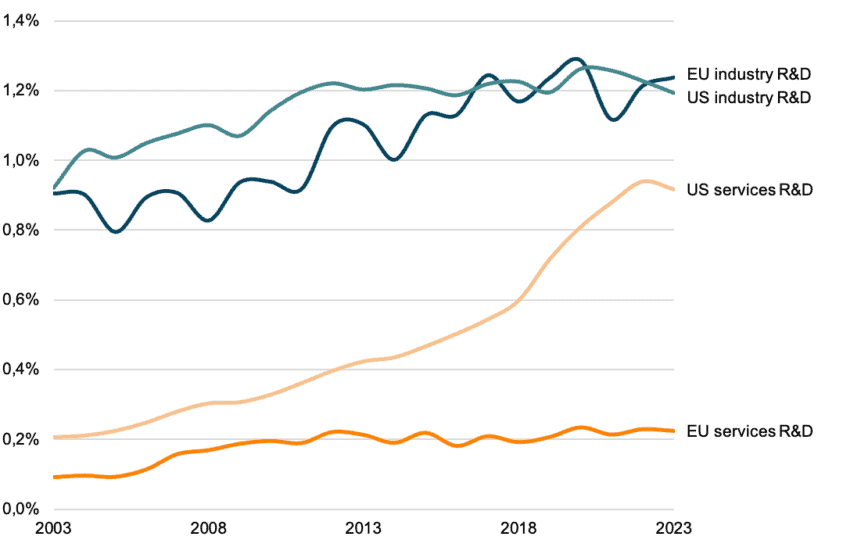

While Europe has kept up with the US on industrial R&D, when it comes to services, the continent has fallen dramatically behind. A €14 billion Transatlantic gap in services R&D in 2003 has ballooned to almost €200 billion today.

To put the gap in perspective: each year, US services firms invest in R&D the equivalent of New Zealand’s GDP. Europe’s services sector invests about as much as Libya’s.

Figure: Europe’s innovation gap is in services, not in industry – Corporate R&D spending (percentage of GDP)  Source: ECIPE based on EU Industrial R&D Investment Scoreboard.

Source: ECIPE based on EU Industrial R&D Investment Scoreboard.

Consulting firm McKinsey estimates that by 2040, sectors like cloud computing, autonomous mobility, AI, space, and biotechnology could make up 16 per cent of global GDP – nearly double the share of today’s leading manufacturing industries, from industrial electronics to semiconductors.

All these sectors rely on services-driven R&D. But European firms still treat it as an afterthought, something to bolt on rather than build around.

Take Volkswagen. For years, it has been Europe’s largest R&D spender. Yet it missed the shift to electric vehicles, assuming Elon Musk would handle the software while Wolfsburg focused on scale. The company’s bet was on tacking services onto steel; an obvious strategy for a traditional manufacturing behemoth.

But the order should have been reversed: build scale through software, then add the hardware. By failing to turn its cars into a services-layer business, Volkswagen remained anchored in a 20th-century model while Tesla built a 21st-century one.

Europe still has a window to close its innovation gap, before it hardens into a vicious circle of Member States further splintering the Single Market.

Innovation drives integration. A serious push on services-focused R&D would give policymakers the leverage to advance deeper integration and blunt nationalist economic pressures.

Where Europe had manufacturing champions pushing for continent-level integration, it had no equivalent in services. Europe’s Single Market for services wasn’t killed by Member States; it was never fully born. Too little innovation ever demanded its survival.

Europe urgently needs an industrial policy for services, in addition to completing its Single Market architecture and unifying its capital markets.

However, that runs counter to its current trajectory. Between 2016 and 2019, 67 per cent of EU state aid went to industrial firms, while just over 30 per cent supported businesses in the services sector. That balance must shift.

Europe now faces a choice. It can keep funnelling money into a manufacturing nostalgia that employs barely 15 per cent of its workers. Or it can finally build an industrial policy for services by investing in skills at scale and backing intellectual property rather than simply subsidising chips and batteries.

“Europe is a continent of industrial production”, Ursula von der Leyen declared in February. That remains true – and should remain so. But a serious agenda for services R&D is not a sideshow. It should be the backbone of Europe’s new industrial strategy.

Ultimately, services are where Europe either catches up – or gets left behind.